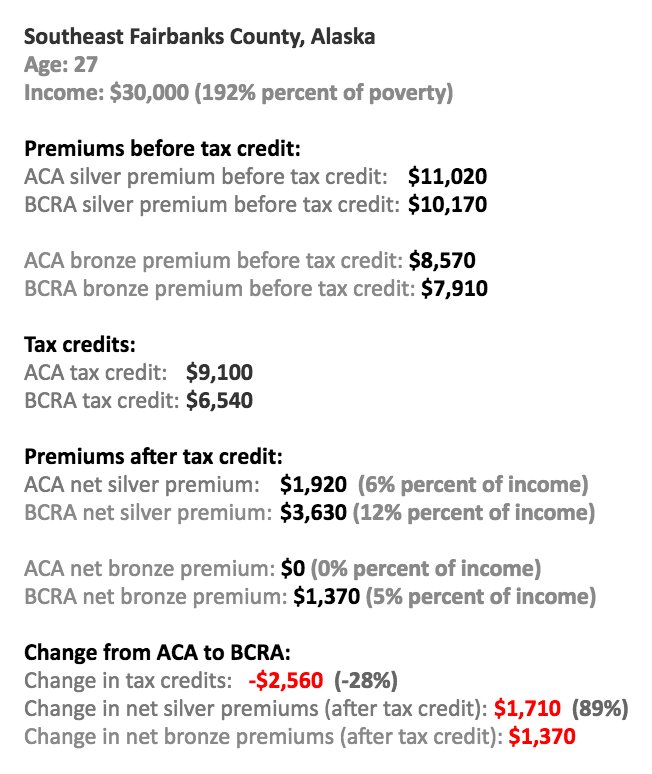

Usually, federal guarantees of health benefits are hard to unravel, especially when a critical mass of the middle class relies on them. But the ACA's complexity has made it much harder to defend politically. If the GOP were about to end Medicare, outraged resistance would swamp them. But the proposed ACA & Medicaid cuts will affect diverse groups in diverse ways. Sure, you can argue to a middle class 27-year-old in Alaska that her premiums will likely increase if something like the BCRA passes:

But there are other millennials whose incomes will be boosted by the program. The ACA's microtargeted, shifting aid for premium assistance tax credits and cost-sharing reduction payments are not easy to rally around. Capitalizing on a steady erosion of social solidarity, the GOP is betting that the issue will barely be salient by November, 2018.

The same logic of fragmentation applies to the regulation of employer-sponsored insurance. Progressive groups are, rightly, sounding the alarm about the likely return of annual and lifetime limits on coverage if something like the AHCA or BRCA passes. But conservative policy analysts can easily respond: "sure, but premiums will in general be lower if insurers are not stuck paying for the highest cost cases. So invest those savings and, voila! you may just have enough money to pay for care even if it's not covered by insurance."

Experts in health policy know just how disingenuous such a pitch can be in a country where median wealth is about $45,000 per adult (and where the putative savings on employer-sponsored insurance via skimpier plans could just as easily be absorbed by employers and their shareholders/bondholders, as by workers). But it's a predictable feint on a Sunday talk show or Twitter beef, one that easily lures a half-conscious press to throw up its hands at the supposed hypercomplexity of health policy and distributional politics. Why not cover the latest Trump tweet instead?

Avoiding the Same Mistakes

Of course, the filibuster-proof majority necessary to pass the ACA was evanescent and fragile. Key senators like Max Baucus and Joe Lieberman were beholden to the insurance industry. There is no need to re-litigate what could have been done better in 2009-10. But we can learn from the past about how technocratic neoliberal health policy backfired, and what a robust future health policy would look like.

President Obama touted the ACA as a plan drawn right from the Heritage Foundation's playbook, its principles already embraced by Mitt Romney in Massachusetts. Classic conservative health policy buzzwords dominated the legislation: competition and marketplaces for insurers, "skin in the game" for the exchange enrollees (especially those in high-deductible plans), targeted aid to conserve government resources. (Even Medicaid was subject to many of these pressures, thanks to the growth of Medicaid managed care.) The ACA encouraged citizens to see themselves as consumers first, carefully parsing health plans for the best deal. Targeted aid was a form of noblesse oblige. The administration's economists (Orszag, Furman, Gruber, etc.) all focused more on "bending the cost curve" than improving the experience of the insured. By jettisoning a public option, Democrats in Congress put their faith in the power of private insurers to control costs while maintaining quality. And the Obama Administration fiercely fought legal challenges to the adequacy of Medicaid reimbursement.

All of these were own-goals. If you continually tell people that 30% of spending on health care in the US is a total waste (rather than misallocated, and ideally re-allocated to health care research and lower-paid workers in the sector), you help justify radical cuts to government subsidies for care. When you train exchange "shoppers" not to pay a penny more for insurance than they need to, don't be surprised when political opponents goad them to stop paying for benefits they may not need. If you trivialize low Medicaid reimbursement rates in court filings, it's a lot harder to go before voters and lament the AHCA/BCRA's slashing cuts. And why tout the magic of the market when those same market actors play hard-ball to water down regulatory requirements and hike premiums right before an election?

A cowed retreat from universalism has made the difference between ObamaCare and Trump/Ryan/McConnellCare seem, to too many, a difference in degree, not kind:

We now know:

1) Private insurers are not going to put on an effective opposition to the gutting of measures like the ACA. They secretly opposed it in 2009. Anyone see any "Harry and Louise" ads in West Virginia, Nevada, or Alaska, to try and save it now?

2) A president can easily sabotage regulation and financing arrangements as complex as those in the ACA. So, too, can Congress make superficially marginal changes that ultimately doom the program--and may be politically rewarded for doing so.

3) Partisan identification has become so stable and intense that failures of the health care system, whatever their cause, are subject to radically different interpretations by different sets of voters. As Jack has observed, "members of each party increasingly view the other as mortal enemies. Polarization, in turn, sows increasing distrust, continuing the cycle." In such a political environment, aspirations to bipartisanship look like little more than excuses for inaction.

4) Diffusion of responsibility (federal/state, public/private, government/contractor) undermines accountability: every player can pass the buck to another.

So the game has changed. The next step for Democrats is to debate the merits of several versions of universal coverage. How about a public option for anyone not covered by employer-sponsored insurance? We already "pay for national health insurance without getting it," as Woolhandler & Himmelstein put it. California politicians have advanced a single-payer proposal. Though vetoed, Nevada's plan for Medicaid buy-in offered another way forward. And somehow nearly every country in Europe figures out a way to get everyone covered.

Will these plans necessitate higher taxes? Sure. But they'd give untold peace of mind to everyone. Some of the top 0.01% may quake with anger at taking home 20 instead of 25 million dollars a year. Less rarefied 1-percenters won't be happy, either. But the average household may find the transition a wash, paying a few thousand more in taxes and a few thousand less in premiums, deductibles, co-insurance, and other out-of-pocket costs. That is no more a recipe for political disaster than letting the status quo continue to be undermined by politicians whose work is premised on the incompetence of governmental authorities.

Moral, economic, and even politico-pragmatic considerations now weigh overwhelmingly in favor of health policy that is simpler and less targeted than the ACA. Whether it's a public option, Medicare-for-all, or single-payer will be up to Democratic primary voters. Policy intellectuals should get on this train, rather than trying to figure out how to tweak the ACA. Too many assumed that Obamacare's carrots and sticks would generate buy-in from stakeholders that could counter predictable opposition in the legislative, executive, and judicial branches. We now know that is wrong: even if no legislation passes this year, executive branch action and inaction can wound the ACA with a thousand cuts. The question now is whether Democrats can deflect the worst of the AHCA/BCRA, while uniting behind a plan more robust, comprehensive, and politically popular than the ACA.

Image credits: KFF (Chart 1); Matt Bruenig (Chart 2).